Economic policy / Macroeconomic Indicators, Economic Growth

This section reports on economic policy initiatives of the Czech government, the EU, and other entities that have a direct impact on the competitiveness of the country. It also includes information on economic priorities of the AmCham and other leading associations.

Show subcategories ▾

Spotlight issue

Inflation in the Czech Republic accelerated again

The month-on-month rise in consumer prices was twice as fast as expected in July. The year-on-year inflation rate reached 3.4%, which is 0.4pp above the CNB forecast, and is heading for 4%. Above all, the prices of services are rising. Concerns about rising inflation expectations will lead the CNB to further raise interest rates. Uncertainty about price developments in the near term remains elevated.

View more

Twitter

Twitter Linkedin

Linkedin Facebook

Facebook Google+

Google+

The CNB continues to tighten monetary policy

As expected, the central bank raised its key repo rate from 0.50% to 0.75% at its August meeting. Although the bank board discussed a 50bp hike, as proposed by the new CNB forecast, in the end it preferred a gradual normalisation of monetary policy. According to Governor Rusnok, the CNB should continue to pursue gradual normalisation for the rest of the year. While the CNB forecast calls for a repo rate of 1.50% at year-end, we expect 1.25% due to the cautious approach of central bankers. However, we already expect a repo rate of 2.25% for end-2022, while the CNB expects 2%. The difference is mainly our expectation of a stronger economic recovery, with a slightly weaker koruna.

View more

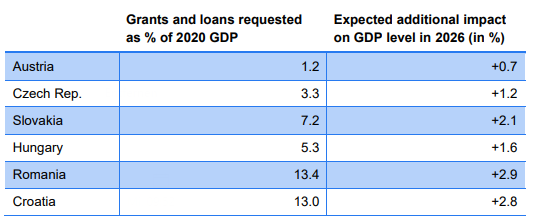

Outlook: EU Recovery Fund set to further strengthen CEE’s economic upswing

CEE economies expected to post GDP growth between 3.7% and 6.9% in 2021

EU Recovery Fund promises to boost GDP levels in 2026 by additional 0.7% to 2.9%

Required structural reforms may trigger increased investment and co-financing

Erste Group outlook: significantly higher full-year earnings expected in 2021

View more